Emergency Fund: How Much, Why & How Fast? Complete Guide

Let’s be honest for a moment. Most people talk a lot about investing, stock markets, mutual funds, crypto, and becoming financially free, but very few actually prepare for things going wrong. Life has a habit of surprising us, and not always in a good way. A sudden job loss, a medical emergency, or an unexpected expense can turn everything upside down. That is exactly where an emergency fund quietly saves you.

An emergency fund may not sound exciting, but it is one of the smartest financial decisions you will ever make. It does not make you rich overnight, but it makes sure one bad phase does not ruin your financial life. Think of it as your personal financial safety net, always there when you need it the most.

What Is an Emergency Fund?

In simple words, an emergency fund is money kept aside only for unexpected situations. These are expenses you cannot plan in advance and cannot avoid when they happen. This could be a sudden medical bill, losing your job, a major house repair, or a temporary drop in income if you run a business or work as a freelancer.

What makes an emergency fund different from normal savings is discipline. This money is not meant for shopping, vacations, festivals, or lifestyle upgrades. It is strictly for emergencies. When you follow this rule, the emergency fund does exactly what it is supposed to do: protect you.

Why an Emergency Fund Is So Important

The biggest reason an emergency fund is important is because income is never guaranteed. Even people with stable jobs and good salaries face layoffs, health issues, or company shutdowns. Without an emergency fund, most people are forced to use credit cards or personal loans, which come with high interest and long-term stress.

Another reason is peace of mind. Knowing that you can manage your expenses for a few months even if your income stops gives you confidence. You make better decisions, avoid panic, and do not feel trapped. An emergency fund gives you breathing room when life puts pressure on you.

It also protects your investments. Without an emergency fund, people often sell their investments during market downturns just to survive. This is one of the worst financial mistakes. An emergency fund makes sure your long-term plans stay untouched.

Types of Financial Emergencies You Should Be Ready For

Financial emergencies can come in many forms. Job-related issues like layoffs, delayed salaries, or business slowdown are very common. Medical emergencies are another big reason people struggle financially, especially when expenses go beyond insurance coverage. Family responsibilities, urgent travel, or sudden repairs to your home or vehicle can also create pressure. An emergency fund is meant to handle all these situations without pushing you into debt.

How Much Emergency Fund Do You Really Need?

This is the most common question, and the answer depends on your situation. A simple and widely accepted rule is to keep three to six months of essential expenses as your emergency fund. Essential expenses include rent or home EMI, groceries, utilities, transport, insurance premiums, and basic education costs.

This amount is not meant to support a luxury lifestyle. It is meant to help you survive comfortably while you figure out your next step.

Emergency Fund Calculation Made Easy

Start by calculating how much money you actually need every month to run your life. Be honest here. Once you have that number, multiply it by the number of months you want protection for.

For example, if your monthly essential expenses are thirty thousand rupees, then a three-month emergency fund would be ninety thousand rupees. A six-month emergency fund would be one lakh eighty thousand rupees. This money gives you time, and time is the most valuable thing during a crisis.

Emergency Fund Based on Job Type

Salaried Individuals

If you have a regular job and a fixed salary, you might feel secure, but no job is completely safe. Layoffs and health issues can happen anytime. For salaried individuals, an emergency fund covering four to six months of expenses is a safe target. This gives enough time to find a new job without financial stress.

Freelancers and Business Owners

If your income is irregular, your risk is higher. Freelancers, consultants, and business owners face delayed payments, client loss, and market ups and downs. For them, a six to twelve month emergency fund makes more sense. This buffer allows you to make smart decisions instead of desperate ones.

Emergency Fund Based on Life Stage

In your twenties, responsibilities are usually lower, and recovery is faster, so a three to four month emergency fund can work. In your thirties, expenses and responsibilities increase, making a six-month emergency fund important. In your forties and fifties, health risks and family responsibilities grow, so having nine to twelve months of expenses saved is a smart move.

Where Should You Keep Your Emergency Fund?

Emergency fund money should be safe and easy to access. This is not the place to take risks for higher returns. Savings accounts, liquid mutual funds, ultra-short-term funds, and fixed deposits with quick withdrawal options are good choices.

Avoid keeping your emergency fund in stocks, equity mutual funds, crypto, or long-term locked investments. During emergencies, markets can be down, and selling at a loss can make things worse.

How Fast Should You Build an Emergency Fund?

The sooner you build it, the better. Ideally, you should aim to save at least three months of emergency fund within six months. After that, work towards six months within a year. This might require cutting down on non-essential expenses for a while, but the security it gives is worth it.

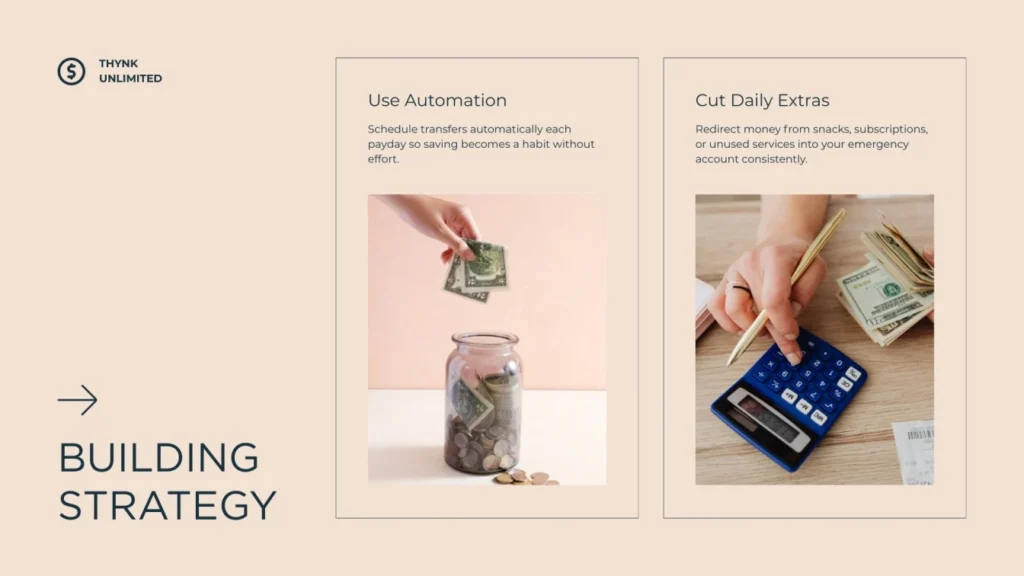

How to Build an Emergency Fund Without Stress

You do not need to save everything at once. Start small and stay consistent. Automating savings right after your income comes in helps a lot. Using bonuses, incentives, or side income to boost your emergency fund can speed things up. The key is consistency, not perfection.

Emergency Fund vs Savings vs Investments

An emergency fund has a very specific purpose. Savings are usually for short-term goals, while investments are meant for long-term growth. Mixing these can create confusion and risk. Keeping your emergency fund separate keeps your finances clear and organized.

What Is a Real Emergency and What Is Not?

Real emergencies are situations that affect your income, health, or basic living needs. Medical issues, job loss, urgent repairs, or unavoidable family responsibilities count as emergencies. Shopping sales, vacations, or lifestyle upgrades do not. Being strict with this rule is what keeps your emergency fund effective.

What to Do After Using Your Emergency Fund

Using your emergency fund does not mean you failed. It means the fund did its job. Once the situation is under control, rebuilding the fund should be your top priority. Redirect your savings until the safety net is back in place.

Common Emergency Fund Mistakes

Many people delay building an emergency fund because they want to invest first. Others keep emergency money in risky assets hoping for better returns. Some use the fund for non-emergencies and forget to rebuild it. These mistakes leave people exposed when they need help the most.

Emergency Fund Myths You Should Ignore

Some people believe insurance is enough and an emergency fund is unnecessary. Others think credit cards can replace emergency savings. Insurance has limits and delays, and credit cards come with high interest. An emergency fund gives instant relief without long-term damage.

A Smarter Emergency Fund Strategy

Once you are comfortable, you can split your emergency fund across multiple safe options. Keeping some money in a savings account and the rest in liquid funds or short-term deposits gives both safety and flexibility.

Review Your Emergency Fund Regularly

Life changes, and so do expenses. As your income grows or responsibilities increase, your emergency fund should be updated. Reviewing it once a year is a good habit.

What is an emergency fund?

An emergency fund is money you keep aside only for unexpected situations like job loss, medical emergencies, urgent home repairs, or sudden travel needs. It is not an investment or long-term savings. The main purpose of an emergency fund is to give you financial breathing room so you don’t have to rely on loans, credit cards, or sell investments when life throws a surprise at you.

How much emergency fund do I really need?

The right emergency fund depends on your lifestyle, income stability, and responsibilities. Most people should aim for at least three to six months of essential expenses. If your income is irregular or you have dependents, a larger buffer may be needed. The idea is to cover basic living costs without stress if income temporarily stops.

Where should I keep my emergency fund?

An emergency fund should be kept in a safe, liquid place where you can access money instantly. It should not be locked into long-term investments or volatile assets. The priority is accessibility and safety, not high returns.

Should I invest before building an emergency fund?

Building an emergency fund should come before most investments. Investing without a safety net increases the risk of withdrawing money during market downturns. A strong emergency fund allows you to stay invested calmly and avoid emotional financial decisions.

Can I use a credit card instead of an emergency fund?

A credit card is not a replacement for an emergency fund. Credit cards create debt and add interest costs, while an emergency fund gives you debt-free protection. Relying only on credit cards during emergencies often leads to long-term financial stress.

Do I still need an emergency fund if I have insurance?

Yes, insurance and emergency funds serve different purposes. Insurance covers specific risks, while an emergency fund handles immediate cash needs like deductibles, delays, or expenses not covered by insurance. Both are essential for complete financial security.

Final Thoughts: Safety Comes Before Growth

An emergency fund may not be exciting, but it is powerful. It protects your lifestyle, your investments, and your peace of mind. Financial freedom does not start with aggressive investing. It starts with safety. Build your emergency fund patiently, respect its purpose, and let it do its job when life throws surprises your way. Your future self will be grateful you started today.

if you want to see how to improve yourself or increase your passive income then click on this links,

Top 10 Life-Changing Books Jo Aapki Thinking Aur Life Dono Badal Dengi

20 Money Habits That Will Make You Rich in 2026

25 Best Passive Income Ideas To Make Money in 2026

Best Stocks to Buy Today (2025) | Top 5 Share For Long Term

Top 10 Greatest Investors & Their Most Powerful Quotes

3 thoughts on “Emergency Fund: How Much, Why & How Fast? Complete Guide”